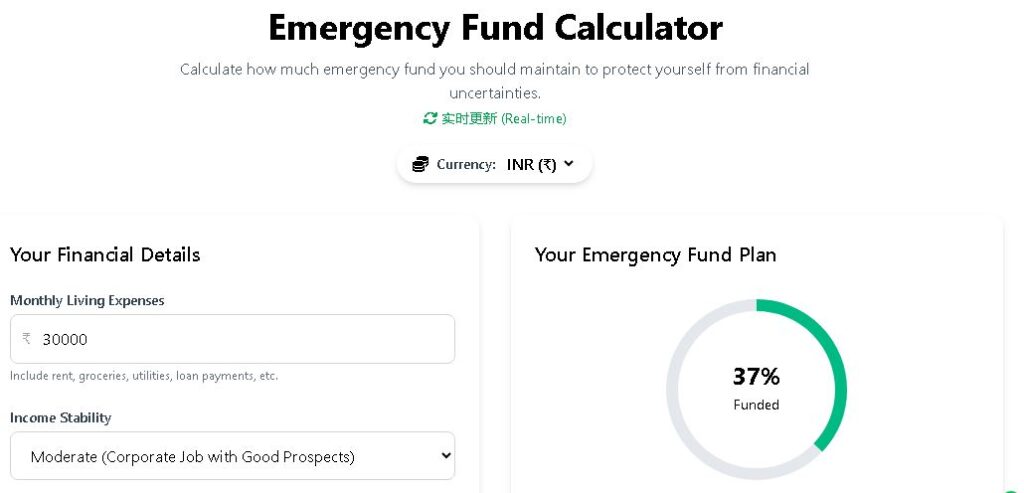

Emergency Fund Calculator

Calculate how much emergency fund you should maintain to protect yourself from financial uncertainties. 实时更新 (Real‑time)

Your Financial Details

Your Emergency Fund Plan

Enter your financial details to calculate your recommended emergency fund.

Recommended Fund

₹0

Current Savings

₹0

Months of Coverage

0

Additional Needed

₹0

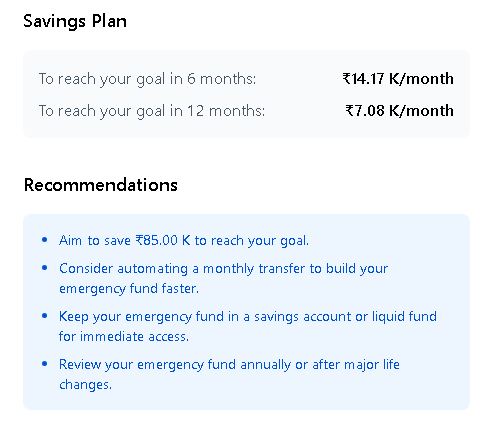

Savings Plan

Recommendations

📘 The Ultimate Guide to Building Your Emergency Fund

Introduction

An emergency fund is your financial safety net – a stash of cash set aside to cover unexpected expenses or a sudden loss of income. Whether it’s a medical bill, a car repair, or a job layoff, having a dedicated emergency fund can mean the difference between a minor inconvenience and a full‑blown financial crisis. Our emergency fund calculator helps you determine exactly how much you should save based on your unique circumstances, and in this article we’ll dive deep into the why, how, and where to store that money. You’ll also discover how to compare different calculators and resources, including those from respected institutions like SBI Mutual Fund, GetSmarterAboutMoney.ca, and HDFC Securities.

What Exactly Is an Emergency Fund?

An emergency fund is a pool of liquid savings that you can access immediately when life throws a curveball. It’s not meant for planned expenses like vacations or down payments; it’s exclusively for true emergencies. Financial planners typically recommend saving between 3 and 12 months’ worth of living expenses, depending on your income stability, number of dependents, and risk tolerance. For example, someone with a stable government job might need only 3 months, while a freelancer with variable income should aim for at least 6 months. This calculator, much like the one offered by Standard Chartered Bank, takes all these factors into account to give you a personalised target.

How Our Emergency Fund Calculator Works

The formula behind the scenes is straightforward but customised: Recommended Fund = Monthly Expenses × (Base Months + Adjustments). We start with a base of 3 months and then add extra months based on your income stability, number of dependents, insurance coverage, and risk tolerance. For instance, each dependent adds 0.5 months, while partial health insurance adds another month. The final multiplier is capped between 3 and 12 months – a range endorsed by many financial experts and used by tools such as the HDFC Securities emergency fund calculator.

Everything updates in real time as you adjust the sliders or type new numbers. You’ll instantly see your recommended fund amount, how far along you are with your current savings, and a savings plan to close any gap. The multi‑currency feature (INR, USD, EUR, GBP, JPY) makes it useful whether you’re planning in Indian rupees or preparing for expenses abroad. It’s a simple yet powerful way to visualise your financial cushion.

Why You Need an Emergency Fund

Without a safety net, an unexpected expense can force you into high‑interest debt or even derail your long‑term goals. Consider these scenarios:

- Medical emergencies – Even with insurance, out‑of‑pocket costs can be steep.

- Job loss – It can take months to find a new role; your fund bridges the gap.

- Home or car repairs – A leaking roof or a broken transmission never comes with a warning.

- Family obligations – Sudden travel or support for a loved one.

Resources like GetSmarterAboutMoney.ca further emphasise that an emergency fund is the cornerstone of any sound financial plan because it prevents you from liquidating long‑term investments at a bad time.

Factors That Affect Your Emergency Fund Target

Your ideal fund size isn’t a one‑size‑fits‑all number. Key influences include:

- Income stability – A stable salaried job requires less buffer than commission‑based income.

- Dependents – More people relying on your income means you need a larger cushion.

- Insurance coverage – Good health and life insurance reduce the amount you need to self‑insure.

- Flexibility of expenses – If you can quickly cut discretionary spending, you may need a slightly smaller fund.

- Risk tolerance – A conservative saver will want more months of coverage than an aggressive investor.

Advanced calculators, such as the one from SBI Mutual Fund, often include additional variables like existing liquid assets and future goals. Our tool focuses on simplicity and immediate feedback, making it easy for anyone to use.

Where Should You Keep Your Emergency Fund?

Liquidity and safety are paramount. The money should be easily accessible without penalty, even if that means earning a lower interest rate. Ideal parking spots include:

- High‑yield savings accounts – They offer better interest than traditional banks and are FDIC/NCUA insured.

- Liquid mutual funds or money market funds – These provide slightly higher returns while still being redeemable in a day or two.

- Short‑term fixed deposits – Good for a portion of your fund, but ensure there’s no exit load.

Avoid investing your emergency fund in stocks or long‑term bonds, as market volatility could shrink your balance exactly when you need it most. The USAA Educational Foundation provides excellent guidance on balancing safety and returns when building emergency savings.

Strategies to Build Your Emergency Fund Faster

If the calculator shows a large gap between your current savings and the recommended amount, don’t panic. Start small and be consistent:

- Automate a monthly transfer from your checking account to a dedicated emergency fund account.

- Direct any windfalls (tax refunds, bonuses, gifts) straight into the fund.

- Cut one or two discretionary expenses – for example, make coffee at home or cancel unused subscriptions – and redirect the savings.

- Set a realistic timeline. Even saving ₹3,000 per month adds up to ₹36,000 in a year.

Many banks offer goal‑based savings plans. For instance, the emergency fund calculator by Standard Chartered can also help you set up a systematic savings plan. Use our tool to track your progress and stay motivated.

Comparing Different Emergency Fund Calculators

No single calculator is perfect for everyone. That’s why it’s wise to cross‑check results. Here’s a quick comparison of some reliable tools:

- SBI MF Emergency Fund Calculator – Integrates with investment planning and provides a detailed breakdown.

- GetSmarterAboutMoney.ca – Offers educational content alongside the calculator, perfect for beginners.

- HDFC Securities – Tailored for investors who may want to link their emergency fund with a brokerage account.

- Standard Chartered Emergency Calculator – Focuses on goal‑based savings and actionable next steps.

- USAAEF Guide to Emergency Savings – Not just a calculator, but a full educational resource on how much to save and why.

Using our tool together with these resources gives you a well‑rounded view of your emergency preparedness.

Frequently Asked Questions

Q: How much should I have in my emergency fund?

A: Most experts recommend 3‑6 months of living expenses. Our calculator personalises this based on your job stability, dependents, and insurance.

Q: Can I use a credit card as my emergency fund?

A: No. Credit cards come with high interest rates and can lead to a debt spiral. A true emergency fund should be cash or cash equivalents.

Q: What if I have debt?

A: Ideally, build a small starter fund (e.g., one month’s expenses) while paying down high‑interest debt. Once the debt is under control, expand to the full recommended amount.

Q: Is it okay to invest my emergency fund?

A: Only if you invest in very low‑risk, liquid instruments. The primary goal is capital preservation, not growth.

⚠️ Important Disclaimer

This calculator provides estimates for educational and planning purposes only. It is not financial advice. Actual emergency fund needs may vary based on personal circumstances, job market, and other factors. Always consult a qualified financial advisor before making significant financial decisions. Finance Toolbajar is not liable for any losses or decisions based on these calculations.

Start building your financial safety net today. Use the calculator above to get your personalised target and begin saving with confidence.